My Real Estate Blog - Market Trends, Tips & Updates

Canada's housing market to stabilize, but don't expect return to "rollicking" price gains, BMO says

1/29/2024 | Posted in Canadian Housing Market by Paul DeAdder | Back to Main Blog Page

Stability is expected to return to the country’s housing market this year as interest rates ease, but homeowners shouldn’t expect a return to the “rollicking” price gains of previous years.

“The Canadian housing market should enter a period of overall stability this year, with lower resale prices, easing mortgage rates and pent-up demand likely helping to set a floor for the market,” writes BMO senior economist Robert Kavcic in a recent research report.

He adds that a return to previous price highs in some locations is “unlikely at this point.”

That’s despite consumer sentiment improving following the Bank of Canada’s latest rate hold and market signals that it’s likely done hiking rates, and a growing expectation from markets that rate cuts will be forthcoming later this year.

Like most big banks, BMO is forecasting the Bank of Canada to lower its overnight target rate by a full percentage point from its current 5.00%.

Downward pressure on prices to continue through spring

Home prices have been trending downward over the past 24 months ever since the start of the Bank of Canada’s rate-hike cycle.

As of December, the national average selling price was $657,145, down roughly 20% from a peak of over $816,000 reached in February 2022.

Some downward pressure is expected to continue through spring, Kavcic says, particularly in Ontario, which saw some of the heftiest price gains over the course of the pandemic.

That’s in line with the latest forecast from the Canadian Real Estate Association (CREA), which expects the average national price to rise just 2.3% in 2024 to a price of $694,173.

Higher-than-average gains are expected in Alberta, Quebec and most of the Atlantic provinces, while CREA sees prices remaining flat in British Columbia and Ontario.

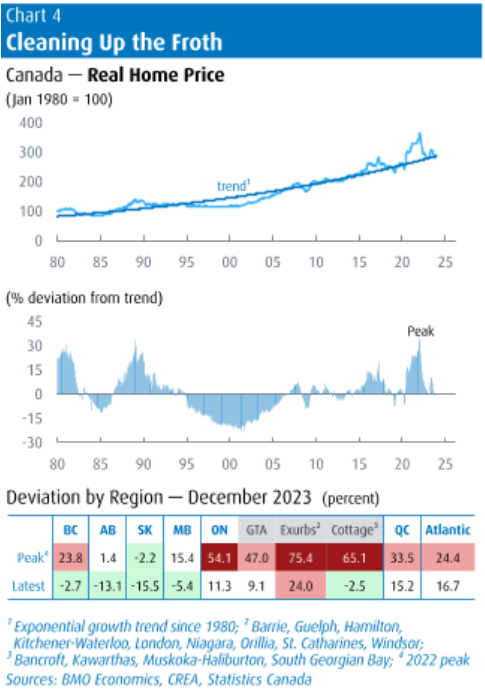

“In real terms, Canadian home prices have now largely adjusted back to their long-term growth trend, suggesting that most froth has been cleaned out of many markets,” Kavcic wrote.

Lingering affordability challenges

Despite the pullback in home prices, high interest rates have essentially cancelled out any benefit in affordability for buyers, observers say.

RBC economists noted that any price recovery will be “restrained by lingering affordability issues.”

National Bank’s Housing Affordability Monitor also recorded a “significant deterioration” in affordability as of the third quarter, which roughly coincided with a peak in bond yields and thus fixed interest rates.

“While still rising income was a partial offset in the third quarter, it did little to assuage the situation,” they wrote. “Looking ahead, we see a moribund outlook for affordability. At the very least, a further worsening is in the cards for the last quarter of the year.”

Since then, fixed mortgage rates have pulled back somewhat, but it will take further declines, including anticipated Bank of Canada rate cuts later this year, to make any kind of meaningful improvement for homebuyers.

“Affordability remains strained, which will limit the scope of any rebound [in home prices],” Kavcic says. “We estimate that the current outlook for lower interest rates will go about halfway to restoring affordability to pre-pandemic levels, while the rest will require either further price declines or (more likely) stagnant prices and a catch-up in incomes.”

The good news, he adds, is that the market is still showing few signs of forced selling.

Source: Canadian Mortgage Trends